Addressing Drawdowns with Data-Driven Efficiency

The 30% drawdown came from prolonged trends overwhelming V1’s simpler logic. Using that data, V3 now adjusts effortlessly, combining historical and current inputs for peak efficiency. Those years were turbulent—Russia-Ukraine conflict, bank failures, the FTX collapse, rate fluctuations. Hedge funds posted losses, the S&P 500 went negative in 2022, and banks struggled or failed. My high DD? It was part of the stress test under crisis conditions—not a weakness. Many overlook this when seeking consistency.

Why V3 Thrives Under Tough Conditions

This system thrives under these conditions: higher risk drives greater recovery. With the V3 system, I precisely tailor risk based on each client’s specific tolerance, goals, and expectations. Using the extensive data and insights from V1, I deliver tangible optimization backed by proven results—not empty promises. I don’t rely on outdated, linear stop-loss methods. Instead, I leverage the invaluable experience gained from market conditions where so-called “pros” faced repeated losses, ensuring a system designed to adapt and perform even in the toughest scenarios.

Stress Testing and Risk Management

Stress testing involves running the system without management, but it’s possible to apply simple techniques to reduce high drawdown (DD). This level of risk only happens in extreme worst-case scenarios. On average, DD is much lower—less than half of these peaks. Profits play an important role because they are reinvested or used to strengthen the account, which helps reduce risks over time. For clients wanting extra protection, I can add equity or balance protector to stop trading in high-risk situations. However, with the way this system is designed, these extra protectors are usually not needed.

Forward Testing and Proportional Risk

Even during high stress, risk is proportional to what I’m risking, and the fact that I had time to stress test and observe live is what sets me apart. During that 2021-2024 run, you will see I only managed the EA to stop it; the purpose was either to fix issues with code that might affect future trading or adjust the strategy using new data and everything I was able to observe while the bot traded live. There are small details we can’t observe while backtesting, so forward testing is key.

Breaking Myths and Proving Real Results

As you can see, even with my V1 version, risk is proportional, and that trend was not small and is something I always double-check in new systems and strategies. I use my past experience and scenarios to keep optimizing my system.

I also added extra stress by using cent accounts, which are considered to have the worst spread/slippage conditions, but as you can see, everything is just a myth from gurus and people that don’t execute and trade live. I was able to double money, withdraw real money, and properly test my edge.

Anyone with as little as $250 USD can now benefit from the advantages of algo trading and passive income thanks to my 113-week stress test seeking value. I’m a value provider, one of the best traders in history, and outperforming markets when everyone else is underperforming. There are no better traders than the ones that are making money in current market conditions; note that.

Note on Transparency

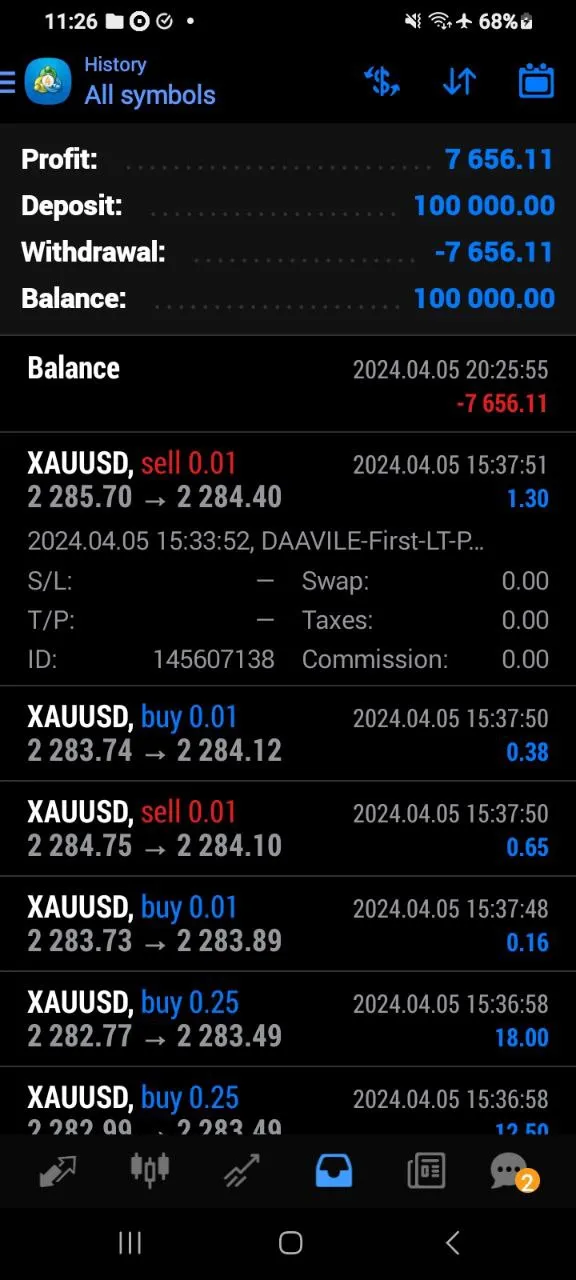

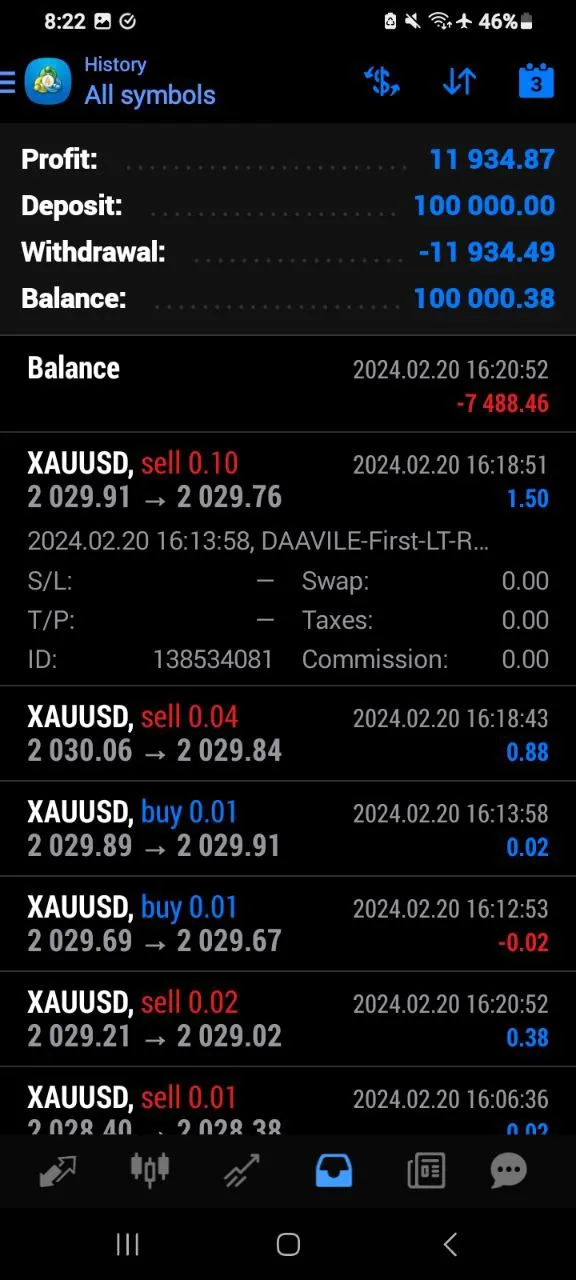

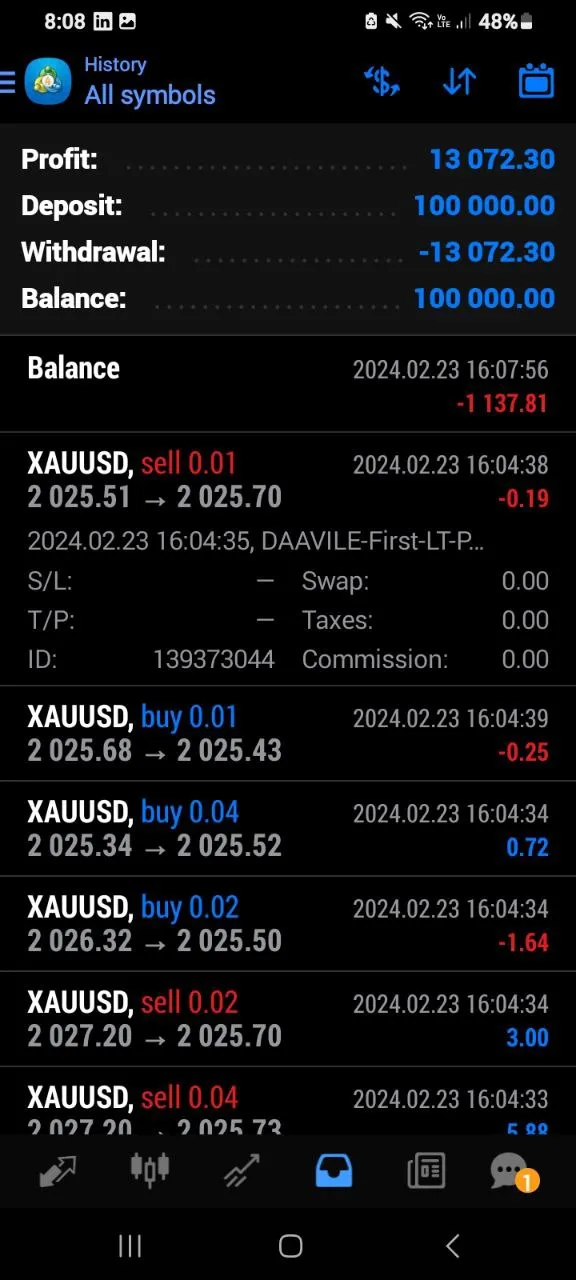

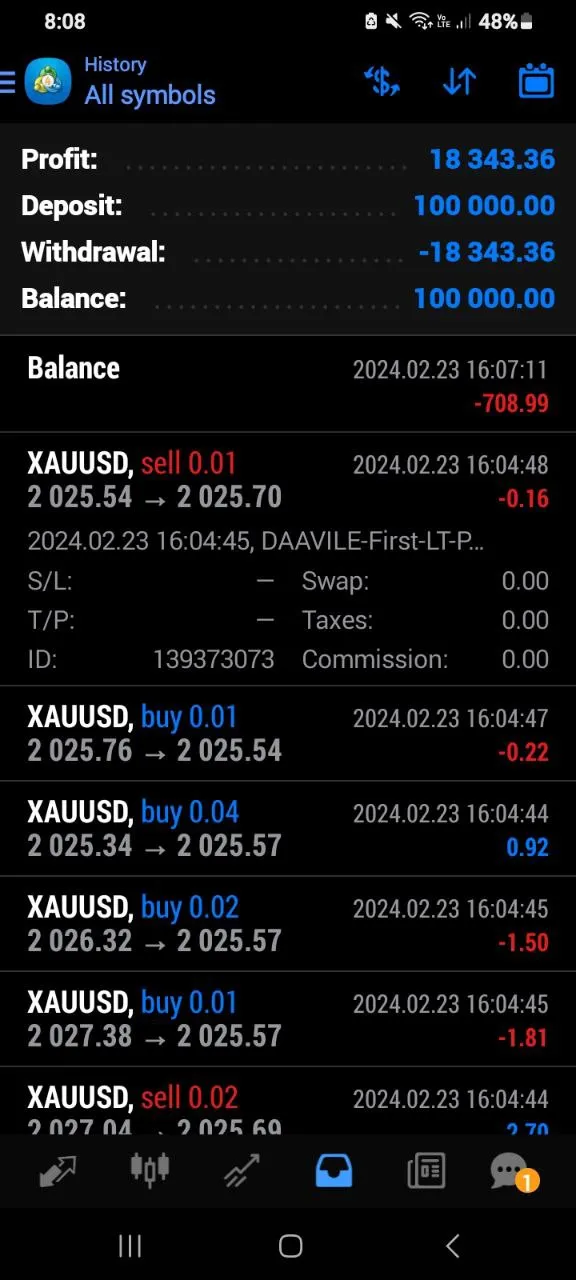

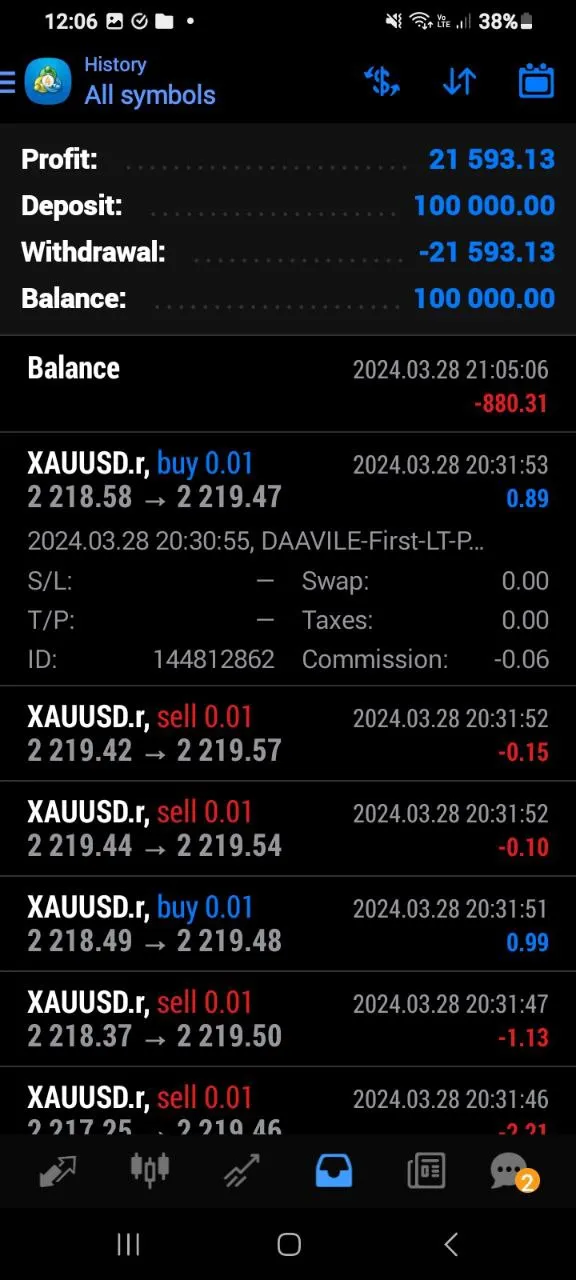

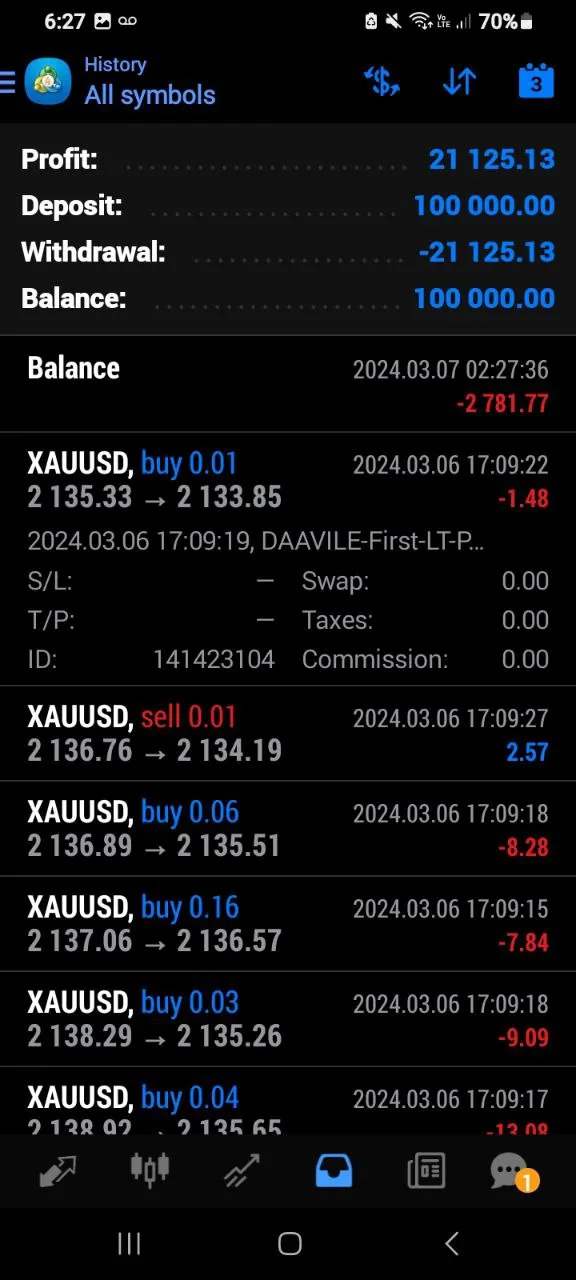

NOTE: Trackers like MQL5 can be manipulated to mislead clients, which is the main reason I share the monthly statements brokers send. In my case, I could mislead clients by showing a 10% DD, while it’s important to understand that the risk was calculated and totaled around 30% of the current balance. Trackers can’t indicate when I’m compounding, so this creates a grey area that we all need to work on explaining to provide full transparency.